GB

GB

US

US

Changes to climate-related financial reporting for Australian organisations

The Treasury has issued final draft legislation requiring major companies and financial entities to report on climate-related financial impacts. Explore the key points including mandatory sustainability reporting alongside annual reports for Group 1 entities.

Important update: Mandatory climate reporting

The Treasury has issued final draft legislation requiring major companies and financial entities to report on climate-related financial impacts.

Key points include mandatory sustainability reporting alongside annual reports for Group 1 entities, introducing new estimation methods and frameworks. This legislation, aimed at supporting Australia's transition to Net Zero, will amend sections of the Australian Securities and Investment Commission Act 2001 and the Corporations Act 2001 (Cth.). Effective from July 1, 2024 for Group 1 entities.

We all know that climate change is impacting companies' financial prospects, resulting in a stronger emphasis on managing and disclosing the associated risks as part of mainstream corporate governance. These risks, alongside the demand for accurate climate disclosures, means businesses and investors must clearly understand and incorporate the financial impacts of climate change into their strategies.

However, despite recommendations from financial regulators, a 2023 KPMG report into Australian companies indicates that while a majority of ASX100 companies acknowledge climate risks, fewer report in alignment with the Task Force on Climate-Related Financial Disclosure (TCFD) standards. There are also a variety of reporting frameworks used and differing levels of accuracy, making it even harder for investors, consumers and government to compare the reporting.

As other countries push forward with their mandatory and standardised climate-related financial disclosure requirements, Australia grapples with ensuring disclosures meet investor needs and are comparably high quality. The challenges to establish a credible, internationally aligned climate disclosure regime will eventually impact our global capital attractiveness.

Australia’s net zero plan

The government’s net zero plan, legislated in 2022, highlights the importance of including disclosures on climate change related risks and opportunities. The disclosures cover how climate change is addressed in corporate governance, how climate related risks and opportunities are managed, and the performance measures and targets applied in managing these issues.

Aims of the amendment bill

In releasing the draft amendment bill, Treasury aims to:

- Improve the quality and transparency of climate-related financial disclosures for shareholders.

- Help regulators manage systemic risks from climate change.

- Facilitate the effective distribution of capital, in line with identified risks and opportunities.

- Establish a credible, internationally aligned climate disclosure regime to enhance Australia's appeal to global investors and align with standards in regions like the EU, UK, New Zealand, and Japan.

Entities included in phase 1

According to Treasury, entities required to lodge financial reports in phase 1 include:

- Listed and unlisted companies

- Financial institutions

- Registrable superannuation entities

- Registered investment schemes

- Large asset owners, including registrable superannuation entities and registered schemes manage funds (exceeding $5 billion)

- Entities that are subject to both the annual reporting requirements under the Corporations Act and emissions reporting obligations under the National Greenhouse and Energy Reporting Act 2007 (Cth) (NGER Act), regardless of size

Exempt entities

- Small and medium-sized businesses, falling below the specified size thresholds

- Entities that are not required to file financial reports under Chapter 2M of the Corporations Act, including those exempt through ASIC class orders or registered with the Australian Charities and Not-for-profits Commission

Phasing of entity reporting

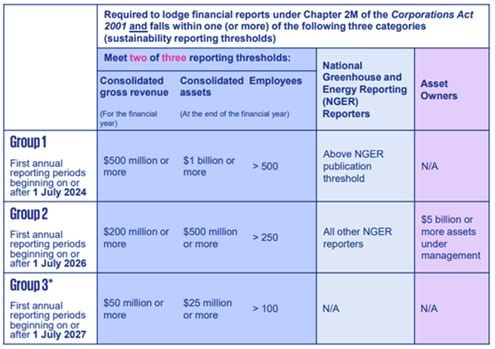

The introduction of mandatory climate-related financial disclosure for entities will be phased across three groups over a span of four years, as detailed in the following table. As can be seen, the initial start date for Group 1 entities is set for 1 July 2024. The government is seeking input from stakeholders on the possibility of changing the start date for Group 1 entities to 1 January 2025, to potentially enhance the quality of reporting during the transition period.

The phase-in of an entity will depend on its size or emission levels. The table outlines the commencement dates for mandatory disclosure, assuming the entities are required to compile and submit annual reports under Chapter 2M of the Corporations Act and belong to one (or more) of the specified three categories.

- Group 3 entities include entities that are in-scope for reporting but that do not meet the thresholds for Group 2. They would only be required to make climate-related financial disclosures in line with the ASRS, if they face material climate-related risks or opportunities for the financial reporting period. Where Group 3 entities assess that they do not have material risks or opportunities, they would only be required to disclose a statement to that effect. Materiality is assessed in accordance with the sustainability standards reporting requirements.

Climate-related reporting requirements

Entities will now need to prepare a new ‘sustainability report’ in addition to financial statements, as part of their annual financial report. Climate-related financial disclosures will sit within this sustainability report, which will form the fourth report required as part of annual financial reporting obligations and be contained in an entity’s annual report.

Climate-related financial disclosures will incorporate information about an entity’s climate-related risks and opportunities, as required by Australian climate disclosure standards. They will also need to include:

- Information relating to governance, strategy, risk management and metrics and targets will be required from the first year of reporting.

- Climate-related risks and opportunities, including specific greenhouse gas emissions data, starting with Scope 1 (direct emissions) and Scope 2 (indirect emissions) emissions from the first year.

- Scope 3 emission disclosures (i.e. emissions that occur up or down their supply chain and emissions associated with their financing or investment activities) will be required from the second-year reporting. This should represent information that is available at the reporting date without undue cost or effort.

- Where Group 3 entities assess that they do not have material risks or opportunities, they would only be required to disclose a statement to that effect.

Content of sustainability report

The sustainability report consists of:

- The climate statement for the year

- Notes to the climate statement

- Any statements prescribed by the regulations for the year

- The directors’ declaration about the compliance of the statements with the relevant sustainability standards

- An index table that enables users to easily navigate the climate disclosures

Important: The estimation methodologies and frameworks used should be consistent with those included in the National Greenhouse and Energy Reporting (Measurement) Determination 2008 (where available) or the relevant annual National Greenhouse Accounts Factors publication, where entities are reporting Australian-based emissions.

Next steps

It’s important that you are familiar with the implications of this final amendment draft as it may impact on your reporting for the 2024-25 financial year. We recommend the following:

- Review the Exposure Draft - legislation content

- Email us your questions on whether your business is implicated

- Start planning – perform a gap analysis and create a roadmap to identify capacity constraints.

Stay informed on the latest industry developments

Don’t forget to follow us on LinkedIn to get Australian-specific clean energy insights delivered straight to your newsfeed